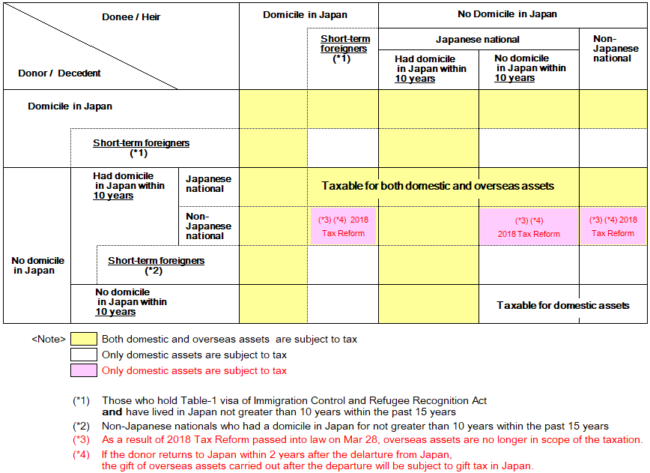

Gift and Inheritance Tax Reform in 2018

According to the 2018 tax reform which was passed into law on Mar 28, non-resident foreigners who inherit/are gifted overseas assets are no longer liable for gift and inheritance taxes for the overseas assets they inherit/are gifted from non-Japanese decedents/donors living outside Japan.

To avoid the gift without taxation by non-Japanese donor leaving Japan temporarily, if the donor returns to Japan within 2 years after the departure from Japan, the gift of overseas assets carried out after the departure will be subject to gift tax in Japan.

Please see below for the detailed information (Please click the chart twice to enlarge).

Last updated: April 19, 2018